News Article

Solar PV Equipment Suppliers in Waiting Mode

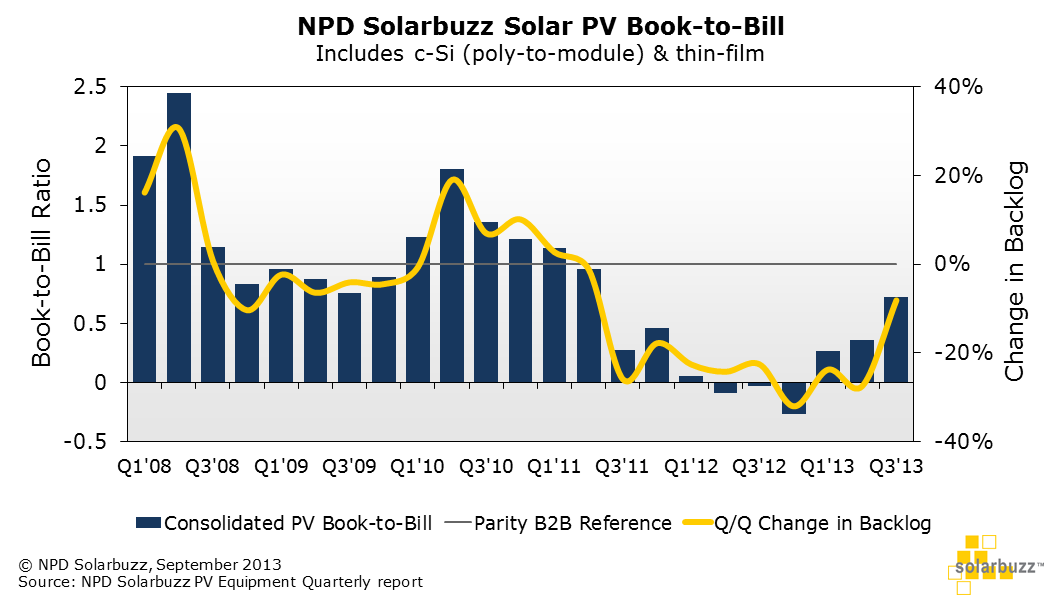

According to the latest information from NPD Solarbuzz, the consolidated solar photovoltaic (PV) book-to-bill ratio is forecast to remain below parity once again during Q3'13, representing the tenth consecutive quarter where net-bookings have been lower than recognized revenues.

The consolidated solar photovoltaic (PV) book-to-bill ratio is forecast to remain below parity once again during Q3'13, representing the tenth consecutive quarter where net-bookings have been lower than recognized revenues.

Finlay Colville vice-president at NPD Solarbuzz stated:

"The PV equipment supply chain continues to be in recession, with the full impact of the shipment deluge of 2011 and 2012 still taking its toll on forward looking guidance. The tool leasing model may provide a short-term boost for domestic Chinese tool suppliers that have finished goods in inventory, but is essentially another factor delaying a meaningful uptick in revenues for PV equipment suppliers."

PV book-to-bill figures held at sub-parity levels for up to 2 years provides further recognition of the prolonged downturn that has impacted on PV equipment suppliers, and is confirmation of the limited capital expenditure (CapEx) that has been released by solar PV manufacturers over the last 18 months.

Directly related to the sub-parity (and even negative) book-to-bill ratios, the PV backlog (overviewed by NPD Solarbuzz as orders that have low risk of revenue recognition 18 months out) is less than 10% of the backlog level accumulated at the end of Q1'11.

A key metric that denotes the bottoming-out point of the CapEx downturn cycle is when the Q/Q change in backlog returns to positive values. This is forecast to occur during the first quarter of 2014. However, the nature of PV CapEx during the next phase of capacity additions by the leading solar PV manufacturers is likely to be very different to previous PV CapEx growth phases:

"¢ The leading PV manufacturers now have different options to increase shipments, either through asset-lite or fabless operations, or simply acquiring excess capacity delivered to competitors during 2011 and 2012 at "˜bargain-basement' CapEx levels.

"¢ Adding capacity with new production tools will be a "˜buyers' market for the next couple of years, with PV equipment suppliers keen to secure new orders at reduced tool pricing levels.

"¢ There are signs emerging of a further threat that could impact PV equipment suppliers during 2014 through the use of tool "˜leasing' options. Here, equipment suppliers deliver process tools to manufacturers (similar to before), but payment terms are staggered with deferred revenue recognition staying on the tool suppliers' backlogs for up to two years.